What Is PMI? How It Works and How to Stop Paying It

By Terry Leinneweber · June 4, 2026

PMI is the extra cost buyers pay when they put less than 20% down. Here's what it costs, how long you pay it, and how to get rid of it.

What Is PMI? How It Works and How to Stop Paying It

PMI shows up on your loan estimate and nobody explains it. You see the line item, you see the dollar amount added to your monthly payment, and suddenly buying with less than 20% down feels like a penalty.

It doesn't have to feel that way.

PMI, or private mortgage insurance, is a real cost, but it's also a temporary one. Once you understand how it works, how much it actually costs, and exactly when it goes away, it becomes a tool you can plan around rather than a surprise that derails your budget. Here's everything you need to know.

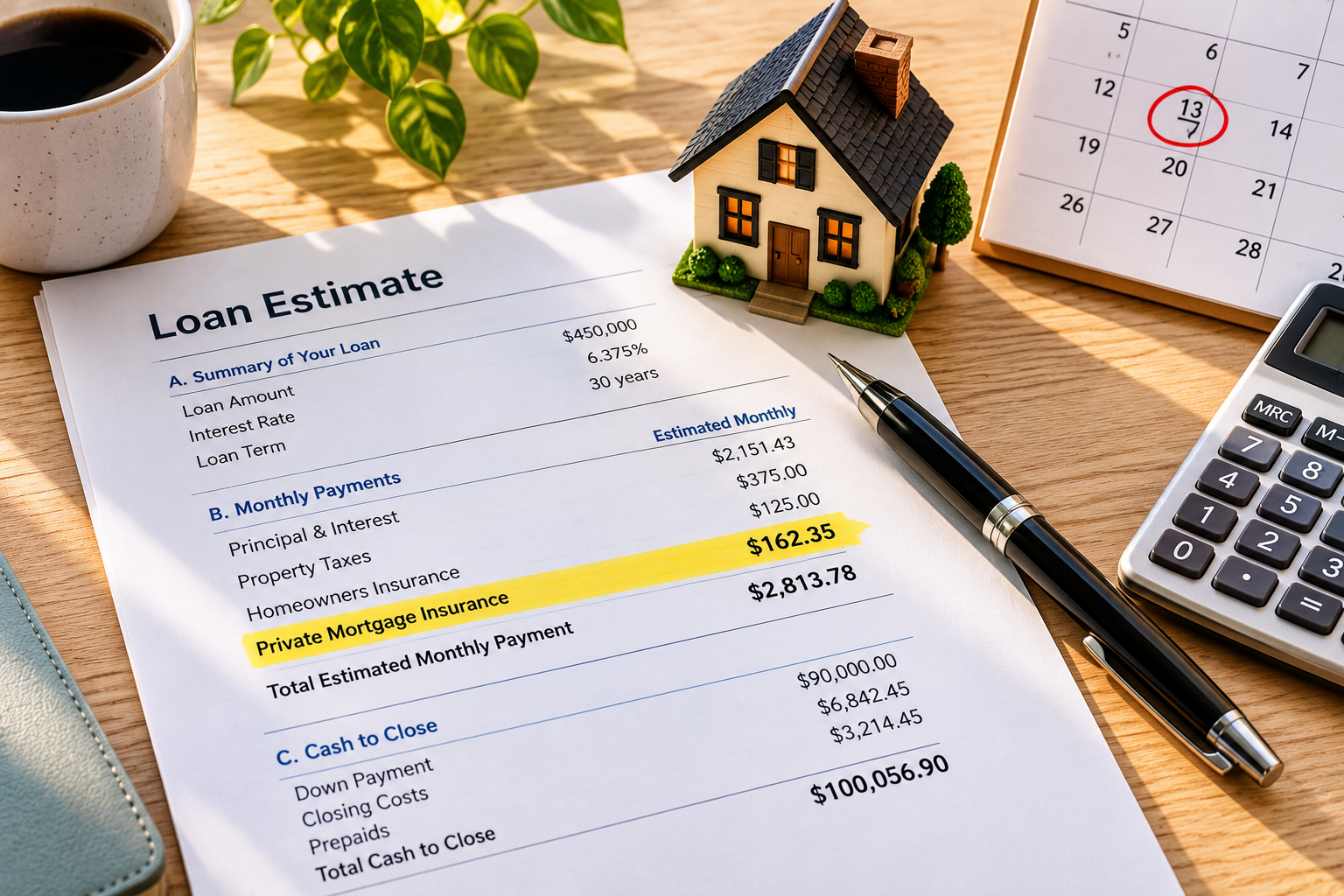

What PMI Actually Is

PMI stands for private mortgage insurance. It's a policy that protects your lender, not you, if you default on your loan.

When you put less than 20% down on a conventional loan, lenders consider you a higher-risk borrower. PMI is how they offset that risk. You pay for the policy, but the coverage runs to the bank.

That said, PMI is what makes low-down-payment homeownership possible. Without it, lenders wouldn't offer 3% or 5% down conventional loans. Think of it as the fee that unlocks the door, knowing you can stop paying it once you've built enough equity.

How Much Does PMI Cost?

PMI typically costs between 0.5% and 1.5% of your original loan amount per year, depending on your credit score, down payment size, and loan term.

On a $400,000 loan, that works out to roughly $2,000 to $6,000 per year, or about $167 to $500 added to your monthly payment.

The higher your credit score and the closer your down payment is to 20%, the lower your PMI rate. A buyer putting 10% down with a 760 credit score will pay significantly less than a buyer putting 3% down with a 640 score.

Your lender is required to disclose the PMI rate in your Loan Estimate. If you don't see it listed, ask.

When Does PMI Go Away?

This is the most important thing to understand: PMI is not permanent.

Federal law, under the Homeowners Protection Act, gives you two pathways to cancel PMI on a conventional loan.

Automatic cancellation. Your lender is required by law to cancel PMI once your loan balance reaches 78% of the original purchase price, assuming you're current on payments. You don't have to ask. It happens automatically.

Requested cancellation. You can request early cancellation once your loan balance drops to 80% of the original value. You can reach 80% through your regular payments, extra principal payments, or a combination of both. Some lenders require a new appraisal to confirm the value hasn't dropped.

On a standard 30-year loan with a 5% down payment, you'd typically hit the 80% mark somewhere between years 9 and 11 through normal payments alone. Making extra principal payments accelerates that timeline.

PMI vs. MIP — They're Not the Same Thing

If you're using an FHA loan instead of a conventional loan, you won't pay PMI. You'll pay MIP, which stands for mortgage insurance premium. They accomplish the same thing but work very differently.

FHA MIP includes two components. The first is an upfront premium of 1.75% of the loan amount, which is typically rolled into the loan. The second is an annual premium, paid monthly, that currently runs between 0.45% and 1.05% of the loan amount depending on your down payment and loan term.

Here's the key difference: on most FHA loans originated after June 2013, MIP stays for the life of the loan if you put less than 10% down. It doesn't cancel at 80% LTV, where LTV means loan-to-value ratio, the percentage of the home's value that your loan represents.

That's a significant long-term cost difference. It's one reason many buyers start on an FHA loan and refinance to a conventional loan once they've built enough equity to drop the MIP entirely.

Four Ways to Avoid or Reduce PMI

Eliminating PMI starts before you close. Here are the most practical options.

-- Put 20% down. The most straightforward path. No PMI from day one. If you can reach 20% through savings, gift funds, or down payment assistance, you bypass it entirely.

-- Use a piggyback loan. Some buyers use an 80/10/10 structure, where a first mortgage covers 80% of the purchase price, a second mortgage (often a home equity line) covers 10%, and the buyer brings 10% as a down payment. This keeps the first loan at exactly 80% LTV, which eliminates PMI. It's not the right fit for every buyer, but it's a legitimate strategy.

-- Choose lender-paid PMI. Some lenders offer to cover your PMI in exchange for a slightly higher interest rate. You don't see a line item for PMI, but you pay for it through the rate. Whether this makes sense depends on how long you plan to stay in the home.

-- Build equity faster. If you're already in a home with PMI, adding even a small amount to your principal each month accelerates your path to cancellation. An extra $100 to $200 per month can shave years off your PMI timeline.

PMI Is a Starting Point, Not a Life Sentence

Most buyers who pay PMI don't pay it for 30 years. Many don't even pay it for 10. Home values in Washington have trended upward over time, which can push your loan-to-value ratio down faster than your payment schedule alone would suggest.

If you bought recently and your home has appreciated, you may already be closer to the 80% threshold than you think. A conversation with your lender, or a licensed broker who can run the numbers, can tell you exactly where you stand.

Want to know whether PMI makes sense for your situation, or whether there's a better structure for your loan? Schedule a free 15-minute call and we'll walk through it.