How Mortgage Amortization Works and Why It Matters for Building Equity

By Terry Leinneweber · June 22, 2026

our mortgage payment stays the same every month but what's inside it changes dramatically over time. Here's how amortization works and how to use it to your advantage.

How Mortgage Amortization Works and Why It Matters for Building Equity

Your mortgage payment is the same dollar amount every single month for the life of the loan. That consistency feels straightforward. What's happening inside that payment, however, is anything but.

In the early years of a 30-year mortgage, the vast majority of every payment goes toward interest rather than reducing your loan balance. In the later years, that ratio flips. The payment never changes, but what it accomplishes changes dramatically depending on where you are in the loan's life.

This is mortgage amortization. Understanding it tells you exactly why equity builds slowly at first, when it starts accelerating, and what you can do to change the timeline.

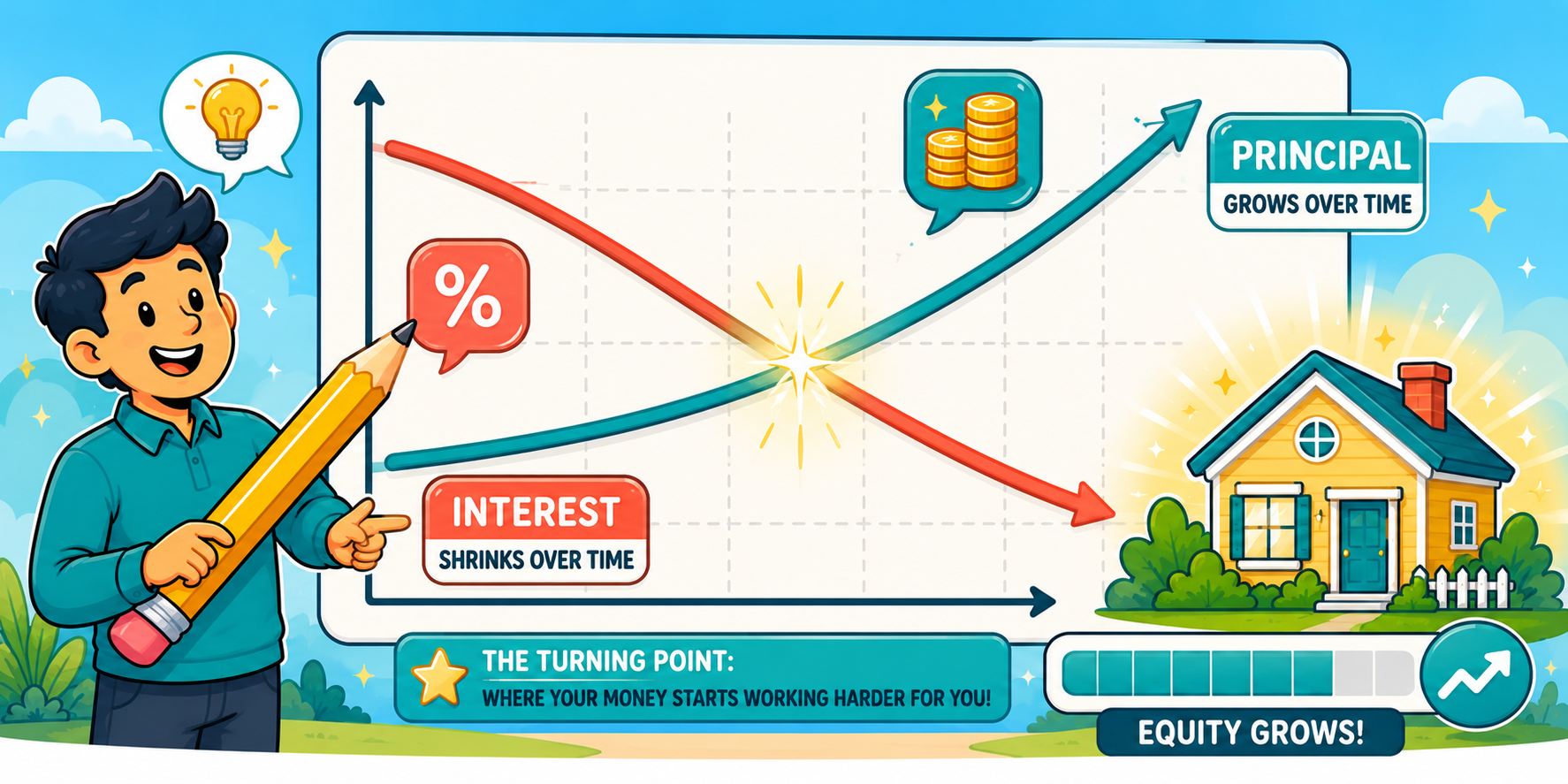

What Amortization Actually Means

Amortization is the process of paying off a debt through scheduled, equal payments over time. Each payment covers two things: the interest owed on the outstanding balance for that month, and a portion of the principal, which is the actual loan balance itself.

The interest portion of your payment is calculated each month by multiplying your outstanding loan balance by your monthly interest rate. As your balance decreases, the interest owed decreases with it. Because your total payment stays fixed, the amount applied to principal increases by the same amount that interest decreases.

This creates a curve. In the earliest payments, interest dominates. By the final payments, almost the entire payment goes to principal. The crossover point, where your principal payment finally exceeds your interest payment, happens roughly halfway through the loan term on a standard 30-year mortgage.

What the Numbers Actually Look Like

The best way to understand amortization is to look at a concrete example. Consider a $450,000 loan at a fixed rate. In the first month of repayment, roughly 80% or more of the payment goes to interest and less than 20% reduces the principal balance. The exact split depends on the interest rate, but the principle holds across rate environments.

By year five, the split has shifted slightly but not dramatically. The loan balance has decreased, but slowly. By year ten, the shift is more noticeable. By year 20 the curve is steep and the majority of each payment is reducing the balance. By years 28, 29, and 30, almost every dollar of the payment is principal.

This is why buyers who sell or refinance in the first five to seven years have built far less equity through their payments than they often expect. The payment history feels significant. The balance reduction is not.

What drives equity growth in the early years is not payment history. It is home appreciation and down payment, not principal reduction.

Why This Matters for PMI Cancellation

If you're paying private mortgage insurance, understanding your amortization curve tells you exactly when you'll reach the thresholds that allow cancellation.

PMI on a conventional loan can be requested for cancellation once your loan-to-value ratio, which is your outstanding balance divided by the home's original value, reaches 80%. It cancels automatically by law when the ratio reaches 78%.

Because principal reduction is slow in the early years, reaching 80% LTV through payments alone on a loan with a small down payment can take nine to twelve years on a 30-year mortgage. Home appreciation accelerates that timeline, but the payment schedule alone moves it slowly.

Knowing your amortization schedule tells you precisely when you'll hit each threshold through payments alone, and how much extra principal you'd need to add to reach it sooner.

How Extra Principal Payments Change the Equation

The most powerful thing a homeowner can do to shift their amortization curve is make extra principal payments. Even modest additional principal payments made consistently can produce dramatic results over a 30-year horizon.

Adding a fixed extra amount to principal each month, say $200 or $300, does two things simultaneously. It reduces the balance faster than the amortization schedule alone, which decreases the interest charged in every subsequent month. And because the interest component shrinks faster, more of every regular payment goes to principal automatically. The effect compounds.

On a $450,000 loan, an additional $300 per month applied consistently to principal can reduce the loan term by several years and save a significant amount in total interest paid over the life of the loan. The exact figures depend on the rate and starting balance, but the directional math is consistent: front-loading principal saves you money at the back end at a ratio that substantially exceeds the nominal extra payment.

There are two important caveats. First, confirm your loan has no prepayment penalty before making extra principal payments. Most conventional, FHA, and VA loans do not, but verify with your servicer. Second, ensure extra payments are applied to principal specifically rather than being treated as an advance on next month's payment. Call your servicer or note it clearly in writing or online payment instructions.

15-Year vs. 30-Year: What Amortization Reveals

The choice between a 15-year and a 30-year mortgage is fundamentally an amortization decision. A 15-year loan amortizes twice as fast. Every payment carries a higher principal component because the balance must be eliminated in half the time.

The trade-off is a significantly higher monthly payment. The 15-year rate is typically lower than the 30-year rate, which partially offsets the shorter term, but the payment is still meaningfully higher.

What buyers get for that higher payment is a dramatically different amortization curve. Equity builds faster. The total interest paid over the life of the loan is a fraction of what a 30-year loan at even a lower rate would accumulate. And the loan is paid off in half the time.

For buyers who can genuinely afford the higher payment without straining their monthly budget, the 15-year loan is a powerful wealth-building tool. For buyers who need the flexibility of a lower payment, a 30-year loan with intentional extra principal payments can approximate a middle path.

How to Read Your Own Amortization Schedule

Every mortgage comes with an amortization schedule, which is a table showing every payment you'll make, what portion goes to interest, what portion goes to principal, and what your remaining balance will be after each payment.

Your lender can provide this at closing. It's also easy to generate with any online mortgage calculator by entering your loan amount, rate, and term.

Reading your own schedule does three things. It gives you a realistic picture of how quickly your balance decreases in the first several years. It shows you exactly when significant equity thresholds are reached. And it makes the impact of extra payments visible in concrete numbers rather than abstract encouragement.

Most buyers never look at their amortization schedule. The ones who do tend to make more intentional decisions about extra payments, refinancing timing, and how to think about the equity in their home as a long-term asset.

Amortization Is the Engine Under Your Mortgage

You don't need to memorize the math to use it well. You need to understand the shape of the curve: slow equity growth early, accelerating equity growth later, with every extra principal dollar you add shifting the curve in your favor.

That understanding changes how you think about your mortgage from a monthly bill you pay into a financial instrument you can manage strategically.

Want to see your specific amortization curve and talk through whether extra payments or a different loan structure makes sense for your situation? Schedule a free 15-minute call and we'll walk through the numbers with you.