Debt-to-Income Ratio Explained: What It Is and Why It Controls Your Approval

By Terry Leinneweber · June 3, 2026

Your DTI ratio determines whether a lender will approve your mortgage. Here's how it's calculated, what limits apply, and how to improve yours.

Debt-to-Income Ratio Explained: What It Is and Why It Controls Your Approval

Your credit score gets all the attention. But there's another number that quietly controls whether you get approved for a mortgage, and a lot of buyers don't know it exists until it's a problem.

That number is your debt-to-income ratio, or DTI. It's the percentage of your gross monthly income that goes toward debt payments. Lenders use it to decide how much mortgage you can actually handle, and in many cases, it's the ceiling that limits how much home you can buy, even when your credit looks great.

Understanding DTI before you apply gives you time to work with it. Here's everything you need to know.

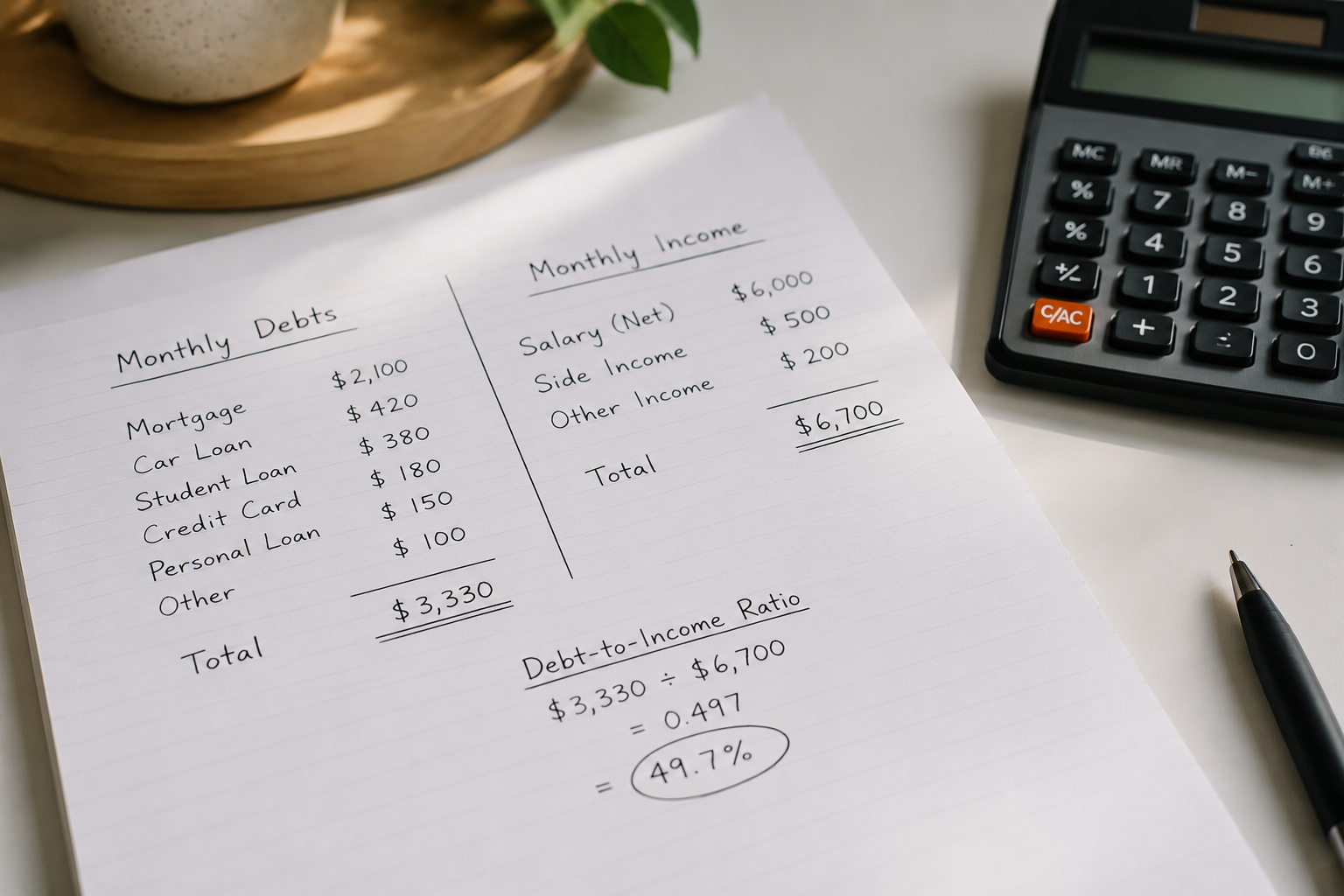

How DTI Is Calculated

The math is simple. Add up all of your required monthly debt payments, divide by your gross monthly income, and multiply by 100 to get a percentage.

Gross income is your income before taxes. Monthly debt payments include anything that shows up on your credit report with a required minimum payment: car loans, student loans, credit card minimums, personal loans, and any existing mortgage.

Here's a basic example. Say your gross monthly income is $7,000. Your monthly debt payments are $500 for a car loan and $200 in credit card minimums. That's $700 in monthly obligations. Divide $700 by $7,000 and you get 0.10, or a 10% DTI.

Now add the proposed mortgage payment. If your new principal, interest, taxes, and insurance payment would be $2,100 per month, your total monthly obligations become $2,800. Divide that by $7,000 and your DTI is 40%.

That 40% is the number your lender evaluates.

Front-End vs. Back-End DTI

Most lenders look at two versions of your DTI, and it helps to know the difference.

Front-end DTI covers only your proposed housing costs, meaning your mortgage principal, interest, property taxes, homeowner's insurance, and any HOA dues. This is also called the housing ratio.

Back-end DTI covers your total monthly obligations: everything in your front-end calculation plus all other debt payments. This is the number most lenders focus on and the one that most often creates qualification issues.

When someone says your DTI is too high, they almost always mean your back-end DTI.

What DTI Limits Apply to Each Loan Type

Each loan program sets its own DTI ceiling. Here's where the major ones land.

-- Conventional loans typically allow a maximum back-end DTI of 45% to 50%, depending on your credit score, down payment, and compensating factors. Strong credit and significant reserves can sometimes push that limit slightly higher with automated underwriting approval.

-- FHA loans generally allow DTI up to 43% with manual underwriting, and up to 57% in some cases when the loan receives an automated approval and the borrower has strong compensating factors. FHA is more flexible on DTI than most buyers expect, which is part of why it's popular with first-time buyers carrying student loan debt.

-- VA loans don't set a hard DTI maximum, but a DTI above 41% typically triggers a residual income analysis, where the lender verifies that you have enough money left over each month after all obligations are paid to cover basic living expenses. VA underwriters care about what's left, not just what's going out.

-- USDA loans generally cap DTI at 41%, though exceptions are possible with strong credit or significant compensating factors.

-- Jumbo loans are the strictest. Most jumbo lenders want to see a back-end DTI no higher than 43%, and many prefer 38% to 40%.

The Most Common DTI Problem Buyers Run Into

Student loans are the most frequent culprit. Even when a loan is deferred or in income-based repayment, lenders still count a payment against your DTI. For conventional loans, they may use 1% of the outstanding balance as the assumed monthly payment if your actual payment is zero or below a threshold. On a $60,000 student loan balance, that's $600 per month added to your DTI calculation, regardless of what you're actually paying.

Car loans are the second most common issue. A $600 monthly car payment on a $7,000 monthly income consumes nearly 9% of your DTI before your mortgage is even factored in.

The gap between what buyers think their DTI is and what lenders calculate is often the difference between a smooth approval and a stressful last-minute scramble.

How to Lower Your DTI Before You Apply

If your DTI is too high, you have two levers: reduce your monthly obligations or increase your gross income.

Paying off a credit card balance doesn't help unless you close the account or the minimum payment disappears from your credit report. What helps is eliminating the monthly minimum entirely, whether by paying it off, consolidating it into a lower-payment structure, or paying it down far enough that the minimum drops.

Here's the practical move most buyers overlook: call your lender before you apply. Share your full financial picture, including every debt. A good broker runs your DTI in advance and tells you exactly which accounts to address first, in what order, and what impact each change will have on your approval.

That conversation takes fifteen minutes. It can save you months of guessing.

DTI and Affordability Are Not the Same Thing

This is worth saying plainly. Qualifying for a certain DTI doesn't mean you should max it out.

Lenders approve loans based on what you can technically qualify for. They're not factoring in your childcare costs, your aging parents, your plans to change careers, or how much you want to keep investing each month. A 45% DTI is legal. It's not always smart.

A mortgage payment that leaves you cash-tight every month is a financial strain that compounds over time. The goal isn't to buy as much house as a lender will approve. It's to buy the right amount of house for your actual life.

Know Your Number Before You Apply

DTI is one of those things that's easy to fix when you find out about it early, and genuinely difficult to work around when it surfaces mid-transaction. The best time to look at yours is before you start shopping, not after you're in contract on a home.

If you want to know your DTI, what limits apply to the loan type you're targeting, and whether there are any quick moves worth making before you apply, that's exactly what a short call is for.

Ready to get a clear picture of where you stand? Schedule a free 15-minute call and we'll run the numbers with you.