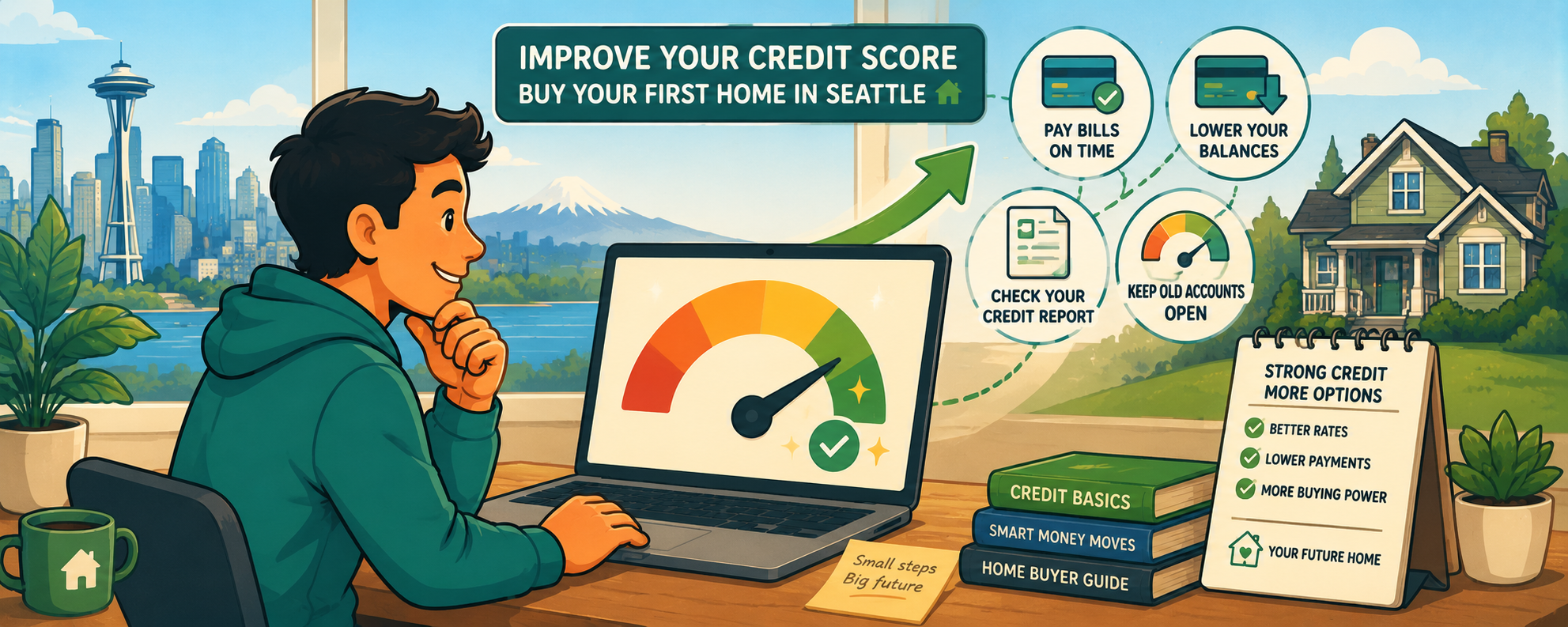

How to Improve Your Credit Score Before Buying a Home

By Terry Leinneweber · May 3, 2026

Your credit score controls your rate, your loan options, and your buying power. Here's exactly how to improve it before you apply for a mortgage.

How to Improve Your Credit Score Before Buying a Home

Your credit score might be the most important number in your home buying journey, and most buyers don't look at it until they're already sitting in front of a lender.

By then, it's too late to fix it.

The good news is that credit scores respond to the right moves faster than most people expect. A focused 6 to 12 month effort can add 50 to 100 points, which can mean a lower rate, a better loan program, and hundreds of dollars less per month on your mortgage payment. This guide walks you through exactly what to do, and in what order.

Why Your Credit Score Matters More Than You Think

Your credit score doesn't just determine whether you qualify. It determines what everything costs.

Two buyers purchasing the same $350,000 home with the same loan amount can end up with dramatically different monthly payments based on credit score alone. The buyer with a 760 score locks in a lower rate. The buyer with a 640 score pays more every single month for the life of the loan.

Here's how the score thresholds break down across common loan types:

-- 580 or above makes you eligible for an FHA loan, a government-backed mortgage with as little as 3.5% down. FHA loans are one of the most accessible paths for first-time buyers.

-- 620 or above opens the door to conventional loan programs, which typically offer more flexibility on mortgage insurance and loan structure.

-- 640 and above starts to unlock more competitive rates and lender options.

-- 740 and above puts you in the top pricing tier, meaning the lowest available rates on most loan programs.

If your score is below 580 right now, you're not ready to apply yet. But you can be. Here's how.

Step 1: Pull Your Credit Report and Know What You're Working With

Before you can improve your score, you need to see exactly what's on your report.

Go to annualcreditreport.com. That's the only federally authorized site for free credit reports. Pull all three, Equifax, Experian, and TransUnion, because lenders typically use the middle score of all three, and errors can appear on one report but not the others.

Look for four things: late payments, collection accounts, high balances relative to your credit limits, and any accounts that don't belong to you. Errors are more common than most people realize, and disputing them is free.

Takeaway: Dispute any inaccurate information directly with the credit bureau reporting it. Removing a false derogatory mark can move your score quickly, sometimes within 30 to 45 days.

Step 2: Pay Down Your Credit Card Balances

This is the fastest lever most buyers have access to.

Credit utilization, which is the percentage of your available credit limit you're currently using, makes up about 30% of your FICO score. Most scoring models reward you for keeping that number below 30%. The sweet spot for maximum score impact is below 10%.

If you have a card with a $5,000 limit and a $3,500 balance, you're at 70% utilization. That's dragging your score down significantly. Paying that balance to $500 brings you to 10% and can produce a noticeable score increase within one to two billing cycles.

Takeaway: If you have cash savings and high credit card balances, paying those balances down before applying for a mortgage is one of the highest-return moves you can make.

Step 3: Stop Missing Payments, on Everything

Payment history is the single largest factor in your credit score, accounting for roughly 35% of your FICO. One missed payment, especially a recent one, can do significant damage.

If you have past late payments, you can't erase them, but you can dilute them. Every on-time payment from this point forward adds positive history. Consistent on-time payments over 12 to 24 months will meaningfully shift the weight of your profile.

Set every account to autopay for at least the minimum due. The goal is zero missed payments from today forward.

Takeaway: You can't fix what's already on your report overnight, but you can control what happens next. A clean 12-month payment streak heading into your application is a strong signal to any lender.

Step 4: Don't Close Old Accounts or Open New Ones

Two common mistakes buyers make right before applying for a mortgage:

-- Closing a credit card they paid off, because they think it looks cleaner. It doesn't. Closing an account reduces your total available credit, which increases your utilization ratio and shortens your average credit history. Both hurt your score.

-- Opening a new credit card or financing a car. Every new credit application triggers a hard inquiry, which temporarily lowers your score. New accounts also reduce your average account age, which is another scoring factor.

In the 6 to 12 months before you apply for a mortgage, keep your credit profile as stable as possible. No new accounts. No closures. No co-signing for someone else's loan.

Takeaway: The best thing you can do for your credit in the months before applying is nothing. Let the positive history accumulate quietly.

Step 5: Address Collections Accounts Strategically

If you have accounts in collections, this is where a conversation with a mortgage professional becomes important before you act.

Paying off a collection account doesn't always improve your score immediately, and in some scoring models it can temporarily lower it by reactivating the account's recency. The strategy depends on the type of collection, the amount, how old it is, and which loan program you're targeting.

Medical collections specifically are treated differently under newer credit scoring models and don't carry the same weight they used to in mortgage decisions.

Takeaway: Don't pay off or settle collection accounts without talking to a loan officer first. The sequence matters, and the wrong move can delay your timeline instead of accelerating it.

How Long Does It Actually Take?

It depends on where you're starting.

A buyer at 620 targeting 680 can often get there in 3 to 6 months with consistent utilization paydown and clean payment history. A buyer rebuilding from 540 targeting 580 may need 9 to 12 months of disciplined work.

The buyers who improve the fastest are the ones who treat their credit like a project with a deadline, not a vague intention. Set a target score, a target date, and check your progress monthly through a free monitoring tool like Credit Karma or the monitoring service on your existing credit cards.

The Bottom Line

Your credit score is not permanent. It's a reflection of recent behavior, and behavior can change.

The buyers who get the best rates aren't necessarily the ones who started with the best credit. They're the ones who took the right steps early enough to matter. Six months of focused effort before you apply can save you more money than years of negotiating on price.

If you're not sure where your score stands or what it would take to get to your target, that's exactly the kind of conversation worth having before you start shopping for homes.

Want to know exactly what score you need, and how close you already are?

Schedule a free 15-minute call and get a clear, honest picture of where you stand and what to do next.