Mortgage Points Explained: Should You Buy Down Your Rate?

By Terry Leinneweber · June 2, 2026

Buying mortgage points lowers your rate upfront. But is it worth it? Here's how to calculate the break-even and decide what actually makes sense.

Mortgage Points Explained: Should You Buy Down Your Rate?

When you're getting a mortgage, your lender will likely offer you a choice: pay a little more upfront and get a lower rate, or keep your cash and take the rate as quoted.

That choice is called buying mortgage points, also known as discount points. And for buyers who don't know how to evaluate it, it's easy to either overpay for something that won't benefit you, or pass on savings that would have paid off significantly over time.

Here's how points actually work, what they cost, and how to know in about five minutes whether buying them makes sense for your situation.

What Are Mortgage Discount Points?

A mortgage discount point is a one-time fee you pay at closing in exchange for a lower interest rate. One point equals 1% of your loan amount.

On a $450,000 loan, one point costs $4,500. In exchange, your lender reduces your interest rate, typically by around 0.25%, though the exact reduction varies by lender, loan type, and market conditions.

Two points would cost $9,000 and might bring your rate down by roughly 0.50%.

The key question is never whether the rate goes down. It always does. The question is whether you'll stay in the home long enough to recoup that upfront cost through lower monthly payments.

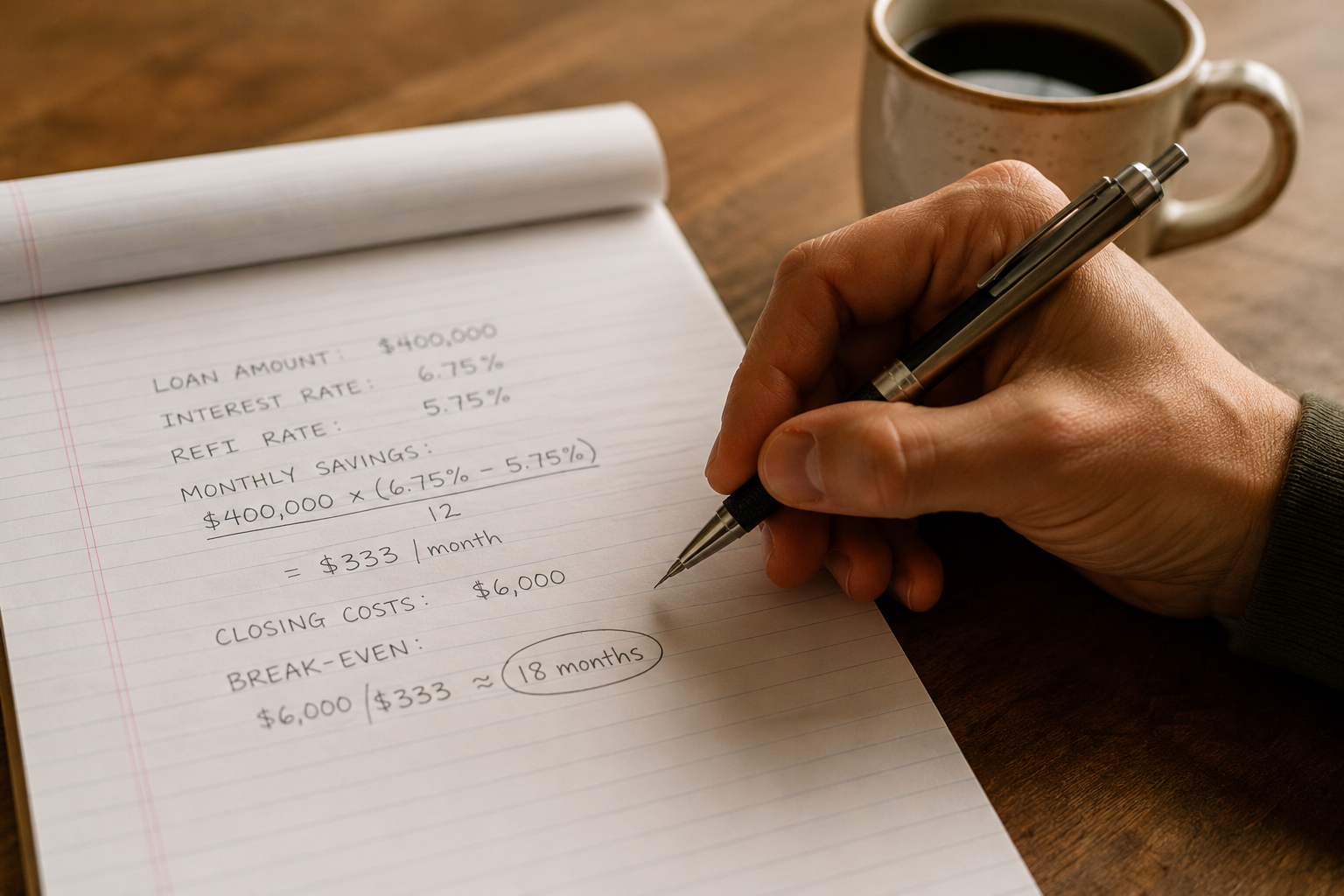

How to Calculate the Break-Even Point

The break-even calculation is straightforward. Divide the cost of the points by the monthly savings they produce. The result is the number of months it takes to get your money back.

Here's an example using round numbers.

You're borrowing $450,000. Your quoted rate without points is 6%. Buying one point for $4,500 drops your rate by 0.25%.

On a 30-year loan, that 0.25% difference saves roughly $68 per month in principal and interest. Divide $4,500 by $68, and your break-even is approximately 66 months, or just over five and a half years.

If you plan to stay in the home longer than that, buying the point works in your favor. If you plan to sell or refinance before then, you come out behind.

This is the only math that matters. Everything else is noise.

When Buying Points Makes Sense

Points are most valuable when two things are true at the same time: you have the cash to cover them without straining your reserves, and you have a clear reason to believe you'll stay in the home past the break-even date.

Move-up buyers who've found their long-term home, buyers purchasing in neighborhoods where they have deep roots, and buyers who plan to age in place are all strong candidates.

If you're buying a forever home and your break-even is four years out, paying points is essentially a guaranteed return. You're not guessing. You're doing arithmetic.

When Buying Points Does Not Make Sense

Points are rarely worth it when you're early in your career, when your household situation may change within the next few years, or when you're stretching to cover your down payment and closing costs.

Draining your cash reserves to buy down your rate is a bad trade. Reserves protect you after closing, for repairs, for income disruptions, for life. A slightly lower rate doesn't help you if a leaky roof empties your savings account six months after you move in.

Points also lose their value quickly if rates drop and you refinance. The moment you refinance, your old loan closes and the savings from those points disappear. You effectively paid for a benefit you didn't fully collect.

If there's any reasonable chance you'll refinance within three to four years, think carefully before buying points.

Discount Points vs. Origination Fees - Know the Difference

These two items often appear near each other on a Loan Estimate, and they are not the same thing.

Origination fees are what lenders charge for processing and underwriting your loan. You pay them regardless of whether you buy points. They don't reduce your rate.

Discount points are optional. They exist solely to lower your rate in exchange for upfront cash.

When you're comparing loan offers from different lenders, look at both categories separately. A lender quoting a lower rate may be building extra origination fees into the deal or requiring you to buy more points to reach that number. The only accurate way to compare is to look at the total cost structure, not just the rate headline.

A Third Option: Lender Credits

Points work in reverse too. Instead of paying more upfront to lower your rate, you can accept a higher rate in exchange for a credit toward your closing costs. This is called a lender credit.

If you're short on cash at closing but can handle a slightly higher monthly payment, lender credits can offset some or all of your closing costs. You pay more over time, but you protect your liquidity at the moment you need it most.

Lender credits are especially useful for buyers using down payment assistance programs, where closing cost cash can be tight even after the assistance is applied.

The Right Answer Depends on Your Numbers

There is no universal rule about whether to buy points. The right answer is personal. It depends on your rate, your loan amount, how long you plan to stay, and how much cash you have available after closing.

What I can tell you is that most buyers either skip this conversation entirely or accept whatever the lender defaults them to without running the math. Neither is a great approach.

If you want someone to run the break-even for your specific loan scenario and tell you plainly whether points make sense in your situation, that's exactly the kind of call worth having.

Ready to see the numbers for your loan? Schedule a free 15-minute call and we'll walk through it together.