How to Choose a Mortgage Lender in Washington State

By Terry Leinneweber · May 21, 2026

Not all mortgage lenders are the same. Here's exactly what to compare, what questions to ask, and why the lowest rate isn't always the best deal in Washington.

How to Choose a Mortgage Lender in Washington State

The lender you choose affects more than your interest rate.

It affects how smoothly your transaction runs, how quickly you close, whether your loan officer picks up the phone when something goes sideways, and whether the loan product you end up with was actually the best one available for your situation. In Washington's market, where a delayed closing or a loan falling apart can cost you a home entirely, those factors matter as much as the rate itself.

Most buyers spend more time choosing their countertops than their lender. This post helps you get that backwards.

Here is exactly what to compare, what questions to ask, and how to know when you have found the right fit.

Step One: Understand the Types of Lenders

Not every lender operates the same way. The three you will encounter most often in Washington are banks and credit unions, direct mortgage lenders, and mortgage brokers. Each has a different structure that affects what they can offer you.

Banks and credit unions originate loans using their own money and their own loan products. If you already have a relationship with a local credit union or bank, that is a reasonable place to get a quote. Some institutions offer rate discounts for existing customers. The limitation is that they can only offer what is on their own shelf. If their products do not fit your situation, they cannot go elsewhere.

Direct lenders are non-bank mortgage companies that originate and fund their own loans. They typically have a wider product range than banks and often invest heavily in technology, making the application process faster and more digital. The same limitation applies: they are selling their own products only.

Mortgage brokers are licensed professionals who work with a network of wholesale lenders, sometimes thirty, forty, or more, and shop your loan across all of them to find the best rate and product match for your specific profile. A mortgage broker acts as an intermediary between you and multiple mortgage lenders, shopping your loan to find the best rates and terms. Brokers help borrowers access more loan options and can be especially valuable for buyers with complex situations, including self-employed buyers, investors, or those needing specialty products like non-QM loans or jumbo financing.

For most buyers in Washington, especially first-time buyers who do not know which loan type or product is best for their situation, a broker offers the broadest access with the least amount of legwork on the buyer's part.

Step Two: Get Quotes from Multiple Lenders

This is the single highest-return action you can take in the mortgage process, and most buyers skip it.

Freddie Mac research shows that getting just one additional rate quote could save homebuyers an average of $1,500 over the life of the loan, and getting five more quotes saved an average of about $3,000.

Buyers who compare offers can save $80,000 or more on average over the life of a 30-year loan, according to a LendingTree analysis. Rates and fees can vary significantly even for the same borrower profile.

Most experts recommend getting at least three rate quotes when you shop for a mortgage. Three is the minimum. Five is better. The work involved in getting an additional quote is small. The savings are real.

One concern buyers frequently raise is that shopping multiple lenders will damage their credit score. This is largely a myth. Multiple credit inquiries within a 45-day period are treated as a single inquiry for scoring purposes, so doing your mortgage shopping within that window has minimal effect on your credit score. Do your comparisons quickly and do not spread the process out over months.

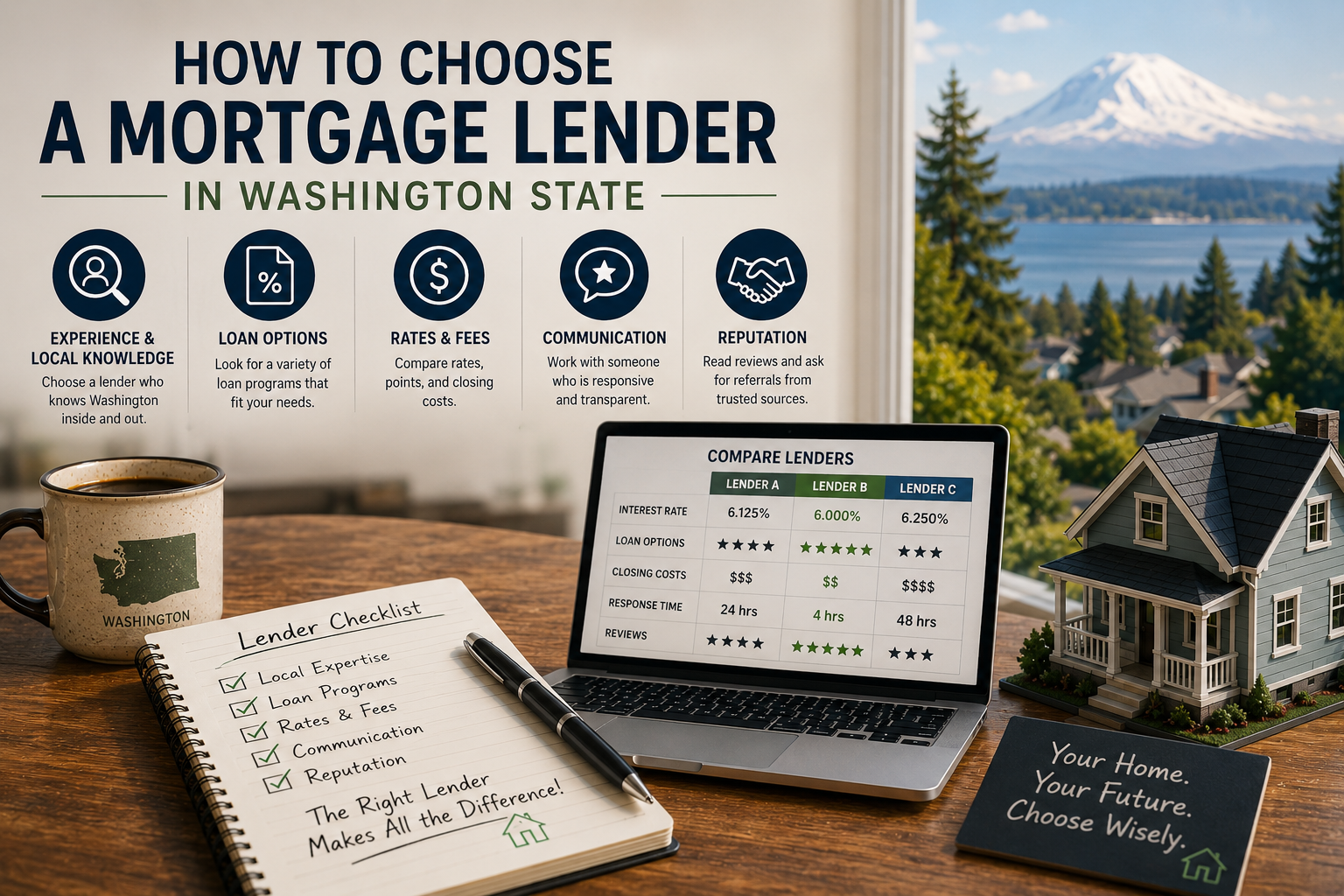

Step Three: Compare the Right Things

This is where most buyers go wrong. They look at the interest rate and stop there. The interest rate is one number. The cost of the loan is a different, more complete number.

APR over interest rate. The most important factor when comparing lenders is the annual percentage rate, or APR, rather than the quoted interest rate alone. APR includes interest, fees, and points, giving you the true cost of the loan. A lower interest rate does not always mean a cheaper loan, but a lower APR does signal a less expensive loan overall.

Total closing costs. Some lenders offer low rates but charge higher upfront fees, which can increase your total cost significantly. A lender offering a rate that looks 0.25% lower than a competitor may be charging $3,000 more in origination fees. You are not getting a deal. You are making a different tradeoff that may or may not make sense depending on how long you plan to hold the loan.

Loan program fit. Not all lenders offer the same loan types. If you know you want an FHA or VA loan, focus your search on lenders who are approved for those programs, since not every lender makes them. If you are self-employed and need a bank statement loan, you need a lender who offers non-QM products. If your purchase price exceeds conforming limits in Washington, which sit at $1,063,750 in high-cost counties for 2026, you need a lender with a competitive jumbo product. Rate shopping across lenders who do not even offer the right loan type for your situation wastes everyone's time.

Closing speed. In Washington's market, the ability to close on time matters. A lender that can get you through the closing process faster can help you win a home in a competitive market. Ask every lender you are considering: what is your average time to close, and what percentage of your loans close on time? A lender with a poor track record on on-time closings is a liability in a competitive offer situation.

Step Four: Use the Loan Estimate as Your Comparison Tool

Once you have submitted applications to two or three lenders, each is required by federal law to send you a Loan Estimate within three business days. This standardized document shows your interest rate, APR, estimated monthly payment, and an itemized breakdown of closing costs.

For each lender you work with, ask for an itemized summary of estimated fees. After you have submitted an application, the lender is required to provide you with a Loan Estimate that includes the terms of your loan, all estimated costs, your APR, finance charges, and payment schedule.

Put your Loan Estimates side by side. Compare the origination charges, the third-party fees, the prepaid items, and the total cash to close. The differences will be visible in black and white. Ask any lender to explain a fee you do not recognize. A lender who cannot clearly explain their own Loan Estimate is not a lender you want managing your transaction.

Because mortgage rates change frequently, it is best to compare loan programs on the same day so that you can accurately judge Loan Estimates from several lenders. A quote from Monday and a quote from Thursday are not a meaningful comparison if rates moved in between.

Step Five: Ask the Questions Most Buyers Never Ask

Beyond rates and fees, a few direct questions will tell you more about a lender than any rate sheet.

Who services the loan after closing? It is common for a lender to sell your loan to a servicer after closing. A loan originator is responsible for creating your mortgage. The servicer is responsible for managing the loan until you pay it off, meaning the servicer is simply who you make your monthly payments to. When you choose a mortgage lender that also services their own loans, you maintain one relationship throughout the life of the loan. If continuity matters to you, ask upfront.

Do you have experience with my loan type? A lender who closes VA loans every week handles the VA appraisal process, the COE, and the BAH income calculation smoothly. A generalist who does one VA loan a quarter handles it slowly and sometimes incorrectly. Specialty matters. Ask how many loans of your type they closed last year.

What does your communication look like during the process? You want to know whether you will have a direct point of contact for your loan, how quickly they return calls and emails, and whether they proactively update you or wait for you to chase them. The answer you get will tell you something useful.

What could delay or derail my closing? A good loan officer can look at your file and tell you exactly where the risks are. If a lender cannot answer this question, they have not thought carefully enough about your situation.

One Washington-Specific Note

Washington has no state income tax, which can simplify income documentation for W-2 earners. But it also means buyers often carry higher gross incomes that push them into jumbo territory faster than buyers in lower-cost states. King County, Snohomish County, and Kitsap County all have elevated conforming loan limits, but buyers targeting the Eastside or waterfront markets may still need a lender with a strong jumbo product and competitive jumbo pricing.

Washington also has a large military population, and VA lending expertise varies enormously between lenders. If you are a veteran, the lender's VA volume and familiarity with VA-specific guidelines, not just their advertised VA rate, is one of the most important factors in your comparison.

The Bottom Line

Choosing a mortgage lender is not about finding the biggest brand name or the lowest advertised rate. It is about finding the lender whose products, pricing, and process match your specific situation and give you the best path to closing on time.

The best lender for you will be the one that offers you some combination of the lowest APR, terms that meet your needs, and convenient and helpful customer service. That combination looks different for a first-time buyer using FHA than it does for a veteran using a VA loan or a self-employed buyer needing a bank statement product. Freedom Mortgage

The only way to know is to compare. Get at least three Loan Estimates. Ask the right questions. And choose the lender who gives you the clearest, most direct answers.

Ready to see how our rates and service compare?

Schedule a free 15-minute call and we will pull a same-day rate quote for your specific loan type, walk through the full Loan Estimate, and answer every question you have before you commit to anything.